How to budget $6,000 per month using the 10-20-70 rule

- Team at LSH

- May 4, 2025

- 3 min read

Any reference to specific products in this article is for informational purposes only and does not constitute an endorsement by Little Success Habits. The information and estimates contained herein does not constitute the provision of financial or investment advice. Conduct research or seek guidance from a licensed financial professional before making investment decisions.

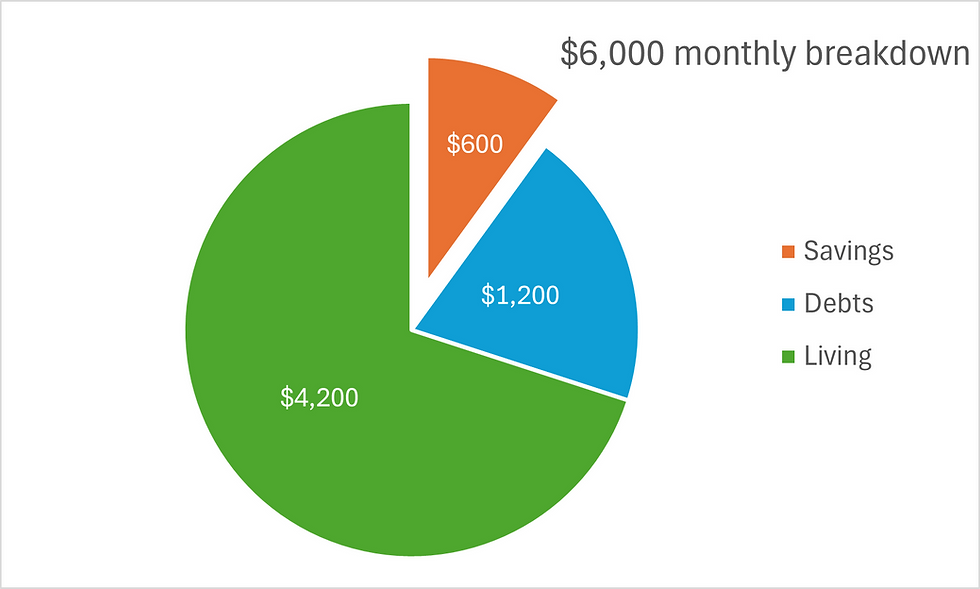

Here is an example of a user of the Summary of the 10-20-70 rule and how they allocate their approximate $6,000/month net income. Why should you use 10-20-70? The plan helps you build wealth and reduce debt immediately. If you save and don’t spend a portion of your money, you will have more money. You will feel like you’re able to save and start building your confidence as you are building the habits. If you allocate 20% of your monthly net income to your debts, pay the minimums on all of them, and any extra up to 20% for the lowest balance, you will be prioritizing and targeting the debts.

Remember the plan breakdown:

10% first to savings. Remember this helps you prioritize yourself, and it develops the habit of paying yourself first.

20% to then pay non-mortgage debts e.g., credit card, student loan, and car loan.

70% for bills, needs and wants e.g., utilities, gas, mortgage and so on.

Using this breakdown, $6,000 per month (or $3,000 bi-weekly income) is allocated as:

10% of $6,000 = $600 to savings e.g., to a High Yield Savings Account (HYSA)

20% of $6,000 = $1,200 to debts like credit card and car loans

You can for example, use the snowball method to prioritize the order of the debts. An example of that is seen in the 'Crushing debt with the Snowball' article.

30% of $6,000 = $4,200 for bills, needs and wants e.g., internet, mortgage or rent, phone, groceries.

The user automatically allocates 10%, 20%, and 70% of their bi-weekly paycheck to the 3 separate accounts through their employer portal.

The order of the plan is important. With the first 10%, you are paying yourself first, not the creditors! If you either manually or preferably automate your savings, you’re building the habit of paying yourself first, the habit of saving 10% of your income, the habit of waiting to spend, and the habit of positive association with unspent money. This user will, as long as the savings aren’t used, at the end of a month, have $600 more than without the plan. The $600 can either be used to build a Starter Emergency Fund or contribute towards the Full Emergency Fund. Spending and then saving what’s left leads to you paying yourself last, and saving is not a priority, if at all.

Then the next 20% to those you owe debts to, and the remaining 70% to live on. The 70% can feel be tough, but it's doable.

This user currently has 2 main debts, a Home Equity Line of Credit (HELOC) on a property and a credit card balance that is being paid off. Using the 10-20-70 plan, $1,200 is available for the HELOC and credit card payments. The minimum payments shown, of course will fluctuate per month, but it is a good estimate going forward. Looking at the balances and the minimum payments below.

Debt | Approximate Balance ($) | Min. Monthly payment ($/mth) |

HELOC | 60,000 | $430.00 |

Credit Card | 13,000 | $400.00 |

Using the snowball method, the priority is the card then then the HELOC. The card can have extra put towards paying that balance off. For example, instead of paying $400/month for the monthly minimum, $770 is paid monthly to focus on and crush the credit card debt first. Note, you’re still making the minimum payment for the HELOC of $430/month. The estimated actual monthly payments are shown below.

Priority | Approximate Balance ($) | Min. Monthly payment ($/mth) | Actual mthly payment ($) |

Credit Card | 13,000 | $400.00 | $770.00 |

HELOC | 60,000 | $430.00 | $430.00 |

|

| Total paid to debts | $1,200 |

There you have it. A breakdown of $6,000 per month allocated into the 10-20-70 plan. Take the example and make it your own. Questions, let us know.

To your success.

Comments